Competition – or development – of EU’s eastern gas supply routes has intensified this year. Both EU/U.S. backed Nabucco and Russia’s South Stream have made deals to guarantee realization of new pipelines until 2015. The EU’s new “southern corridor” – Nabucco as essential part of it – has been dubbed a version of U.S. “Silk Road Strategy” aimed to block Russia from gas fields around Caspian Sea and its connection to Iran. Russia on the other hand wants direct access to EU markets without transit via Ukraine.

Until this summer the gas game has be seen as battle between Russia and West. Now the world economic crisis and current low price of gas have brought a new player to game in fuel sector – China. With its financial strength China has now had ability to intensify its offensive towards the Caspian Sea energy sources especially in Kazakhstan (especially oil) and Turkmenistan (especially gas). Will the outcome be, that both Russia and Western powers with their companies will lose Caspian oil and gas while it will flow to East? Not necessary but from now on one can not ignore China as key player in region.

As main source related to energy game in Kazakhstan and Turkmenistan I have used Ajdar Kurtov’s fine article “SCO Yekaterinburg summit and China’s energy offensive towards the Caspian Sea”

Kazakhstan

Back in the 1990s Kazakhstan made easily available its mineral wealth to American, British, French and Italian companies. The bulk of the profit generated was channeled to Kazakhstan’s new partners. A threat loomed large of Kazakhstan turning into a third-world country with a raw exports role to play for the highly-advanced states.

However, Kazakhstan growing stronger economically, socially and politically while the world hydrocarbons market prices shooting up early this century made Kazakhstan leaders think better of their old stands. The new conditions prompted Kazakhstan to reconsider the earlier signed agreements, and Astana specifically proclaimed the objective of establishing state control over the oil and gas sector. The Kazakh authorities brought pressure to bear on the foreign companies in a bid to force the latter to accept changes to the earlier signed contracts.

The national company “KazMunaiGaz” was made responsible for advancing Kazakhstan’s state interests in the oil and gas field institutionally. Initially Kazakhstan leaders applied much the same tactic to pursue the same objective to one of Kazakhstan’s three oil refineries, the Pavlodar refinery, which is located by the Russian border and technologically oriented to Russian oil refining. The facility was privatized in January 1997 and the government’s stake placed in management by the US CCL Oil Ltd. Company on the terms of a public-private partnership agreement. But the Kazakh government prematurely terminated the agreement a few years later and handed over a 51% stake to the OAO “Mangistaumunaigaz”. The company later brought its stock of shares to 58%, with 42% of the Pavlodar oil refinery’s stock capital owned by the state. After that the national company “KazMunaiGaz” bought 51% of the “Mangistaumunaigaz” stock of shares from Indonesia’s Central Asia Petroleum and consequently gained control over the facility.

It was reported on the 16th of April 2009 that amid the world economic crisis Kazakhstan borrowed from China 10 billion dollars during N. Nazarbayev’s visit to Beijing. The Chinese CNPC Company bought a 50% stake of “Mangistaumunaigaz” for 1.4 billion dollars. Kazakhstan leaders are ousting western partners from the hydrocarbons market and refusing to meet Russian companies halfway, while losing ground to China. Chinese companies already own a third of Kazakhstan-produced oil, or more than 20 million tonnes per year. The purchasing of Kazakhstan’s “Mangistaumunaigaz” assets by China’s CNPC further tightens China’s grip on the Kazakh oil market and weakens the positions of Russia and the West in Kazakhstan’s fuel and energy complex.

Turkmenistan

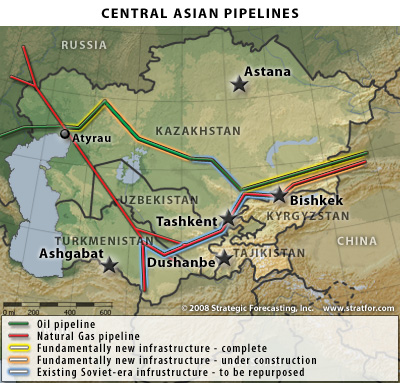

China’s policy of advancing towards the Caspian Sea region resources is seen also in Turkmenistan. Ashgabat has long discussed the construction of a 6,500 kilometer gas pipeline from Turkmenistan to China to Japan. The construction project was due to be carried out in 10 years and was pretty costly (11 billion dollars, of which some 1.7 billion dollars would account for the sea section of the pipeline). Later the easterly direction of Turkmen natural gas deliveries was sort of “updated”, namely the option for laying a pipeline to Japan was dropped, with China having been made the only terminal point of delivery.

A more important development for Turkmenistan in 2006 was the republic’s president S. Niyazov’s visit to China in early April. The main agreement in a package he signed in Beijing was the General intergovernmental agreement on the implementation of the Turkmenistan – China gas pipeline project and on selling natural gas from Turkmenistan to the People’s Republic of China in the volume of 30 billion cubic metres annually for 30 years since the time the gas pipeline was commissioned, which was due in 2009.

The new Turkmenistan-China gas pipeline will be nearly 6,500 kilometres, with over 180 kilometres due to be laid in Turkmenistan, 530 kilometres, – in Uzbekistan, 1,300 kilometres, – in Kazakhstan, and over 4,500 kilometres, – in China. The overall cost of the project makes up some 20 billion dollars. 17 billion cubic metres of Turkmen gas were due to be annually exported through the development of new gas fields, while the remaining 13 billion cubic metres of annual gas exports,- through the construction of gas purification and treatment plants at the largest gas condensate field Bagtyyarlyk.

The construction of the pipeline (Turkmenistan-China) got under way in 2008 when Russian Company “Stroytransgaz” won 395 m€ contract for laying the Turkmen section of project and also plant to purify and dehydrate gas and a gas-measuring station. The Turkmen stage is expected to be finished by December 2009 and the entire pipeline in late 2010.

Iran?

On February 21st 2009 the Iranian and Turkmeni governments signed an agreement that will give Iran the rights to develop the Yolotan gas field in Turkmenistan. The deal will help Iran resolve gas supply problems in its north-eastern provinces. Turkmenistan will sell Iran an additional 350 billion cubic feet of gas annually, more than doubling current supplies of almost 300 bcf a year, according to the agreement first disclosed by Iran’s official media and later confirmed by Turkmenistan.Iran also recently offered to invest $1.7 billion for a 10 percent stake in the second phase of Azerbaijan’s huge Shah-Deniz gas field which will come on line by 2014. Iran already has a 10 percent share in the first phase and it wants to import large volumes of gas from the Azeri field. For Iran, the deals couldn’t be better suited to its objectives. It’s economically unviable currently to supply gas to its isolated, north-eastern third of the country. Getting gas from Turkmenistan would therefore make more Iranian gas available for export to Turkey.

Turkmenistan-Afghanistan-Pakistan-India (TAPI)

The Turkmenistan-Afghanistan-Pakistan-India (TAPI) pipeline on the other hand would feed natural gas into downstream economies that are desperate for natural gas supplies. Afghanistan is the first of these, and energy shortages are rarely discussed as one of the problems of their economy, but with only 10 – 12% of the populace having access to electricity and with only limited natural gas resources (perhaps enough for a 100 megawatt power station), the country needs to import natural gas in large volumes. Pakistan is still desperate for help with natural gas and other energy fuels. But so far there is no pipeline to help.

There is some base to claim that U.S.military’s involvement in Afghanistan is directly related to the large reserves of natural gas in Turkmenistan. While the U.S. military may be a wholly owned subsidiary of the international (i.e. American and British)oil companies), its anyway clear that demand to increase troop levels in Afghanistan jumped a bit along with the recently publicized discovery of the very large large natural gas reserves in the Yoloten-Osman gas field in southern Turkmenistan.

Some (geo)political remarks

* In March 1999, the U.S. Congress adopted the Silk Road Strategy Act, which defined America’s broad economic and strategic interests in a region extending from the Eastern Mediterranean to Central Asia. The act was revised in 2006 to include the energy interests of the US as one of the primary reasons for the US to be in Afghanistan – note no reference to Osama Bin Laden or Al Qaeda ;The Silk Road Strategy (SRS) outlines a framework for the development of America’s business empire along an extensive geographical corridor. The successful implementation of the SRS requires the concurrent “militarization” of the entire Eurasian corridor as a means to securing control over extensive oil and gas reserves, as well as “protecting” pipeline routes and trading corridors. This militarization is largely directed against China, Russia and Iran. More about background of this battle in my article “Is GUUAM dead?”

* As said the new pipeline will run through Uzbekistan and Kazakhstan to Xinjiang in western China. Xinjiang is becoming increasingly important as a transit route for gas pipelines from Russia and Central Asia. Given the vast region’s location several thousand kilometers inside China, it is impractical for the Chinese to protect fully the long stretches of pipelines through Xinjiang’s vast mountains and deserts so they are trying to eliminate the militant groups before the pipelines become operational. So far the unrest in Xijiang has be seen based to ethnic questions. The energy aspect explains why China’s response to unrest is and will be strong also in future.

* Summit of the Shanghai Cooperation Organization that was called in Yekaterinburg on the 16th of June. Besides some universal ideas in statements and declarations the SCO Energy Club has to this day failed to come up with a cooperation model that would suit all member-states. China’s actions on the ground will lay the basis for actual energy cooperation in the SCO framework since instead of some remote private owner China as state (via state-owned company) is implementing the projects. Promoting energy cooperation in SCO framework must from now on take the “Chinese Factor” seriously.

* The bad news for Russia is that there is a customer willing to take all the gas that Turkmenistan has for sale: China. It has been steadily gaining access to the energy wealth of Central Asia, while ousting American, European and Russian companies from the area. Beside oil and gas the Chinese are simultaneously planing to transport also the mineral resources in question to China’s western border.

* For contest between EU’s Nabucco and Russia’s South Stream China’s actions favor later. Today’s arrangements are securing gas for South Stream while Nabucco still is searching supply. It is more clear that Nabucco should be filled with Iraqi and/or Iranian gas and political aspects related to this may delay finding(private) investors and the implementation of project as whole. In bottom line while Russia is taking its part from old gas fields and China from old and new gasfields the Nabucco pipe still is more than half empty.

More about background of Nabucco/South Stream battle in my articles “Is it time to bury Nabucco?” and “EU’s big choice – Nabucco or South Stream?”